16 Jun 2022

Investment markets around the globe continued to grapple with a combination of challenges, resulting in negative market sentiment and severe selling pressure. The Australian market was not spared, with the smaller end suffering the most. In the six weeks to early June, the Australian Emerging Companies index has fallen 17%.

Frustratingly, and disappointingly, the Cyan C3G Fund, which invests predominantly in smaller companies, suffered badly with a fall of 14.0% in May.

Given the recent persistent negative performance of the Fund, we’ll provide some further detail around the issues driving these market conditions, the Fund itself and some forward-looking insights.

Click here for a PDF of this newsletter

Market Conditions

As the world emerges from the pandemic, the global market finds itself facing headwinds including:

- Input costs & inflation– product availability, supply chain constraints, labour shortages and rising commodity and energy prices have all resulted in increased input costs across most industries. These supply issues have resulted in inflationary pressures across almost all developed economies.

- Central bank action – The pandemic-led liquidity binge undertaken by most central banks has come to an abrupt end. The US Fed is now in a quantitative tightening phase. The central banks of most developed economies are trying to find a balance between curbing inflation and not doing too much damage to businesses. The rising interest rate cycle has already begun, but the pace and magnitude is difficult to predict. The RBA took an aggressive stance in June when it recently raised the cash rate by 0.5% to 0.85%.

- Political issues – The Russian Ukrainian war and strained relations with China have created further uncertainty but these concerns appear to have been replaced with those of inflation and rising rates.

The majority of these issues can be largely attributed to the pandemic response by governments and central banks and the subsequent unwinding of quantitative easing. Logistics is improving, supply chains are opening up, costs are still a challenge but will subside as other parts of the supply chain normalise.

The response by the central banks globally indicate a similar stance to the RBA. When the RBA raised rates in early June, it stated:

“Inflation is expected to increase further, but then decline back towards the 2–3% range next year. Higher prices for electricity and gas and recent increases in petrol prices mean that, in the near term, inflation is likely to be higher than was expected a month ago. As the global supply-side problems are resolved and commodity prices stabilize, even if at a high level, inflation is expected to moderate. Today’s increase in interest rates will assist with the return of inflation to target over time.”

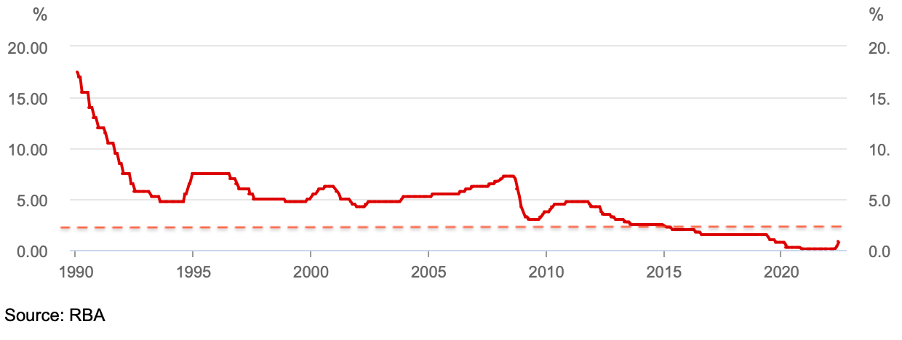

It appears this aggressive or hawkish approach is being used to deliver a quick reversion to the mean. Even if this requires a further 1.5% short-term rate hike, it will have a negative impact on spending and affordability, but in terms of valuing companies on future earnings (which is what the stock market does!), it is far from terminal, or perhaps not even particularly material. The chart below shows the RBA cash rate over time. The dotted line shows where the cash rate would sit if the RBA raised a further 1.5% to sit at 2.35%, barely above pre-pandemic levels. We feel the market is being overly bearish on where long-term rates might land.

Click here for a PDF of this newsletter

Fund Performance in May

At Cyan we invest in emerging businesses that we can understand and directly meet and analyze that have impressive medium to long-term financial prospects. As such we have a growth focus and frustratingly it is growth-focused companies that have been dealt the harshest treatment over the past 8 months. Of course, the market always reacts to macro events, and is doing so now. It also looks forward, so we believe many of the current risks have been priced in, in some cases too drastically, and many quality companies are being sold down aggressively with little focus on the underlying fundamentals.

Performance in May was incredibly frustrating. Not just because share prices were falling, but also because the vast majority of our investee companies have been operating well and delivering positive news in the form of earnings resilience and, in some cases, material new contracts being awarded. All but one of our holdings, Pure Profile (PPL +6%), fell over the month resulting in the overall poor performance.

Some of the companies that were heavily sold down included:

Mighty Craft (MCL –25%) – This alcoholic beverage and venue company faced challenges through lockdown but, like many exposed to hospitality, is recovering strongly. It has developed a strong suite of strategic assets including boutique beer brands, spirits and venues as it builds its strategy of becoming Australia’s leading craft drinks business. It is currently being valued at $70m by the market. It is expected to deliver more than $70m in sales during this Covid impacted year and strong profitable growth in FY23. It acquired the Adelaide Hills Group for $47m last year, which continues to trade well (MCL paid between 6x-7x EBITDA). It is also 37% owner of Australia’s fastest growing beer, Better Beer, which is expected to sell 4m litres in FY22 and upwards of 10m litres in FY23. On those metrics, at $25 per litre of value (which is the general metric for valuing boutique beer brands that reach scale), MCL’s ownership of the brand alone could be worth $90m+. These two assets comfortably exceed the value that is being attributed to whole business at present. Other company assets include other boutique brands such as Jetty Road, Kangaroo Island Spirits and a growing whisky stock.

Kip McGrath Education (KME -15%) – This education and tutoring business operates in Australia, NZ, US, UK and South Africa. It has an enterprise value of $50m, no debt, is cashflow positive, profitable (single digit EBITDA multiple), dividend paying and is expected to grow both revenue and earnings at more than 20% in FY23. It is potentially an M&A target and has recently successfully pushed into the US. The stock is down 40% from its highs of a few months ago and has delivered no negative news.

Raiz (RZI -15%) – This financial investing platform has a current market cap of $70m, with $18m in cash and zero debt (EV $52m). Over the past 12 months it has grown active customers by 50% to around 650,000 who collectively invest more than $1bn (which has grown by over 30% in the last 12 months). The company is profitable in its core operations in Australia and is pushing successfully into South-East Asia. Over the same period, the share price has fallen 60%. As a comparative valuation, Raiz’s US parent Acorns Grow is valued at ~$800/customer. Completely ignoring Raiz’s 350t strong customer base Asia, its Australian business of 290t customers is presently being valued by the local market at just $170/customer and, like KME, we see this as an extremely attractive target for a financial institution.

Touch Ventures (TVL -9%) – The gap between listed investment company TVL’s share price and its NAV (net asset value) has continued to widen to a discount of more than 50%. The company has initiated a share buy-back in May due to the deep value that they currently offer. TVL currently has $79m in cash (or 11cps) which, at current levels, implies a combined value of their existing portfolio of investment assets of around $14m (versus the $94m they have invested and the most recent valuation of these assets of $112m). The share price has fallen 65% since its issue late last year.

We continue to believe in these businesses and will remain invested. Some other of our investee companies that are delivering on their strategies yet have been sold down considerably include Alcidion (ALC -20%), Playside (PLY -6%), Swift Networks (SW1 -10%) and Zoom2U (Z2U -23%).

We have reduced our exposure to Maggie Beer (MBH) as we believe the company faces further operating risks from a pricing perspective into the foreseeable future. We also sold our holding in Universal Biosensors (UBI) as we believe the risk profile and strategy of the business has changed since our original investment.

Outlook

Retail investors have retreated from the market having endured significant losses in recent months. Institutional investors are generally being patient, but trading volumes are low. In fact, last week we had the lowest volume day of 2022, with $4bn worth of shares through the market. That could be considered very quiet through a holiday period, but is quite extraordinary for the last month of the financial year. This means, and particularly at the smaller end where liquidity can be a challenge, that share prices are falling more aggressively than would otherwise typically occur. This is no doubt being exacerbated currently by tax-loss selling before the end of June.

In such markets resilience and discipline are required and we continue to implement the same investment philosophy and process approach that we always have.

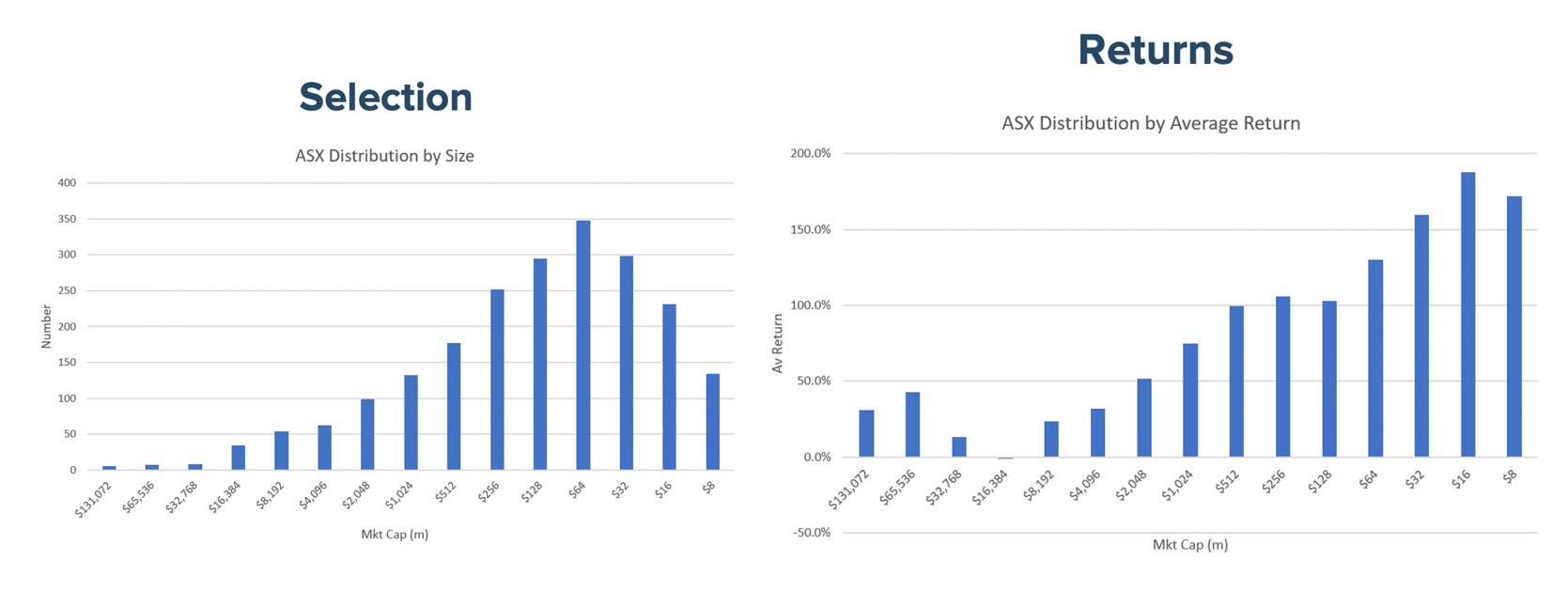

We firmly believe that the most attractive investment opportunities are found outside the Top 100 stocks. The charts below illustrate the distribution of ASX listed companies by size and then by average return relative to size.

There are times when the smaller end of the market is out of favour, particularly in downturns. As most things with markets and economies, it corrects over time and sound investment process, research and risk management will be rewarded.

We currently hold a diversified portfolio containing 23 investments, plus a 16% cash weighting.

To reiterate our recent comments:

“It’s natural to feel impatient or sceptical about the underlying progress our investee companies are making particularly when this is not being reflected in their short-term market prices. However, we’ve been analysing and investing in small caps for almost three decades and know that there are periods of lulls and surges in the marketplace, especially at the smaller end of the market.

Investors may remain wary for some time yet. However, the very best buying opportunities occur when there is pessimism, fear and overwhelmingly negative sentiment, which appears to be the case currently. Whilst we’re not deluded enough to know when to ‘pick the bottom’ it’s clear that there are some increasingly evident gaps between price movements and underlying company performance and value.”

As always if you would like more information about any aspect of your investment, please contact us directly.