10 Sep 2019

We are delighted to report that the Cyan C3G Fund managed to eke out another positive month, rising 0.1% in August. This was particularly pleasing given the weakness in the broader markets which saw the All Ordinaries Index fall 2.2% and the Small Industrials retrace 3.0%. Last month we trumpeted the success of the Fund in navigating weak markets but this is worth addressing again – historically, since inception (as can be seen in the table below) the Cyan C3G Fund has not only fallen far fewer months than comparable indices (17 vs 22-24); when those indices fall, the Cyan C3G Fund falls significantly less on average (-2.1% vs -2.6-2.7%). |

Clearly reporting season meant significant volatility crept into the marketplace with many stocks being subjected to wild price swings. A large cohort of former high-flyers experienced significant pull-backs in the month including: Bellamys (BAL -25%); Speedcast (SDA -60%); Blackmores (BKL -20%); Nearmap (NEA – 20%); Appen (APX -15%); Costa Group (CGC -20%); Magellan (MFG -20%); Platinum (PTM -20%); and Ooh Media (OML -30%). None of these companies are owned by the Fund, but it is a timely reminder that aggressively-priced companies need to continue to deliver ahead of expectations to hold their price in volatile markets. Month in Review

Whilst the Fund did endure some big prices swings, the overall result was a positive outcome. All hail the power of diversification! Perhaps our most pleasing result was that of Quickstep Holdings (QHL). Investors may recall that QHL is a Sydney-based advanced manufacturer of high-value carbon-fibre products, predominantly for the defence industry. We bought into the company in February 2019 and took some additional stock in a placement in March 2019 at which time we wrote about QHL for Livewire. QHL has been listed for 14 years and has never made a profit at the bottom line. Thankfully our timing has been fortuitous and in FY19 QHL posted its first profit of $2.7m on revenues of $73.3m. We fully expect this momentum to continue into FY20 with both organic and new contract revenue growth combined with margin expansion driving further earnings growth. QHL rose 14% in August and with a market capitalisation of $65m (less than the value of its high-margin sales) there appears plenty of upside left in the share price.

Somewhat out of the blue, our best performer of the month was Motorcycle Holdings (MTO) which rose an incredible 65%. This is a company in which we had ridden out quite a bit of pain, with the stock having fallen more than 50% in the past 12 months. Whilst we would typically look to cut underperforming companies, in the case of MTO, much (if not all) of the price weakness was due to appalling market conditions (new motorcycle sales had fallen more than 10%) that saw the stock fall to levels we thought somewhat bargain-basement. Obviously MTO’s FY19 numbers – which reported revenue up 9% and NPAT down 2% (ahead of the industry due to market share gains) – were not nearly as bad as the market had feared and the stock bounced hard and contributed meaningfully to the Fund’s performance in August. We also enjoyed positive financial and share price results from a number of other core holdings that included Afterpay (APT +16%), Atomos (AMS + 7%) and Victory Offices (VOL +5%). On the negative side of the ledger we saw some price pressure in PSI Insurance (PSC -9%) Freelancer (FLN -17%) and Murray River Organics (MRG -8%) but again, due to the diversification of our holdings, these were not significant enough to drive the fund into the red despite the challenging market conditions.

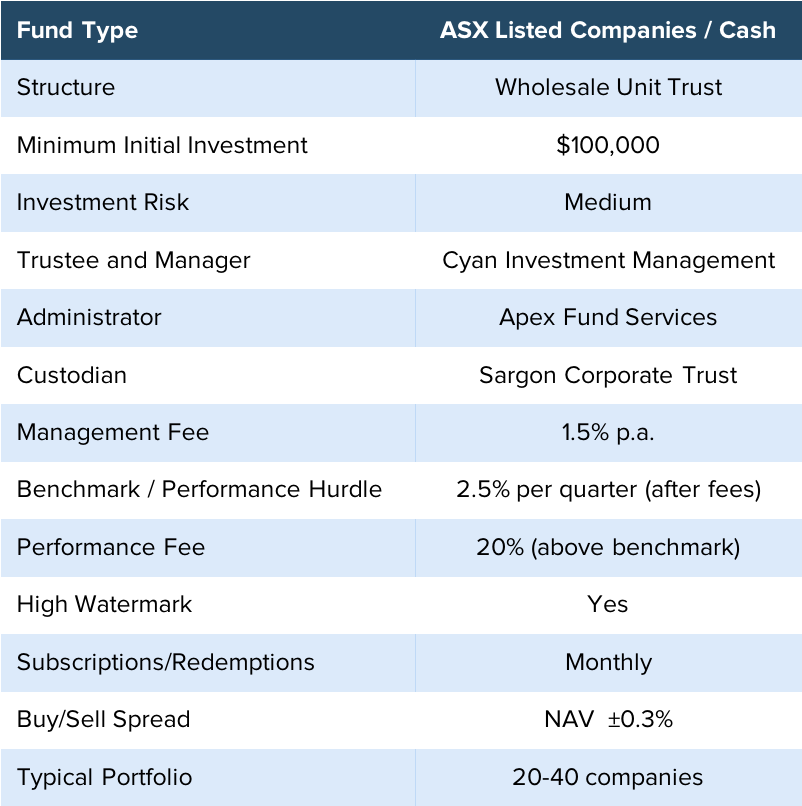

Media We wrote ‘5 beliefs to hold when the market is tanking‘ for Livewire Markets. Mitchell Sneddon of Investsmart’s Eureka Report conducted a fund manager podcast where he spoke to Dean about IPOs, Cyan’s investment process and more. Stockhead spoke with Cyan above what sectors are capturing the market’s attention right now. Outlook It is important to think of an investment in our Fund, indeed any investment in a volatile asset class such as listed equities, as a long-term investment. Yes, we know that is a bit of a cliche, but it really is very difficult, if not impossible, to reliably predict month-to-month movements in the direction of the market or our Fund. We believe our strength is in finding and investing in genuine, exciting and potentially thriving companies; we have less faith in our ability to predict when the marketplace will recognize and appreciate their achievements which is what drives re-valuations in the Fund. However the pipeline of opportunities in our space continues to flow generously and we believe there is every possibility that our current and future investments will generate excellent outcomes for our unitholders. We thank all our investors for their support and look forward to keeping everyone updated with the Fund’s progress. As always we are contactable in person and encourage you to do so if you have any questions for us. Some key Fund criteria are outlined below.

|